Last updated: July 2026

Vendor finance vs bank finance: where the money for your acquisition actually comes from

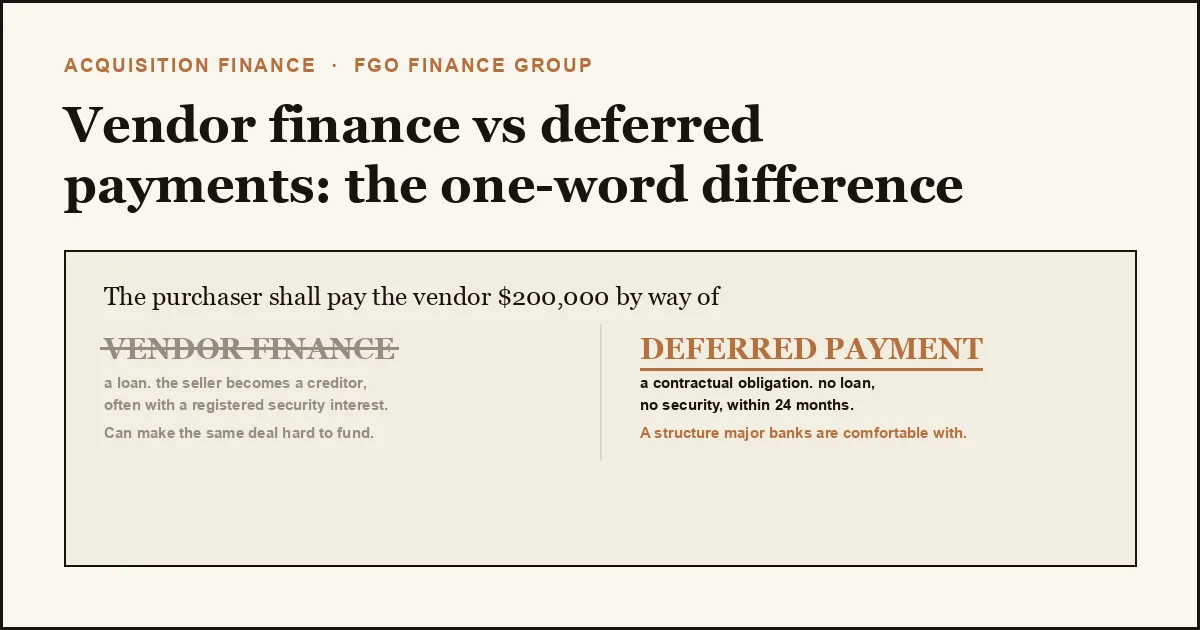

Two comparisons come up constantly on ETA calls, and buyers often collapse them into one question when they answer different things. Vendor finance vs deferred payment is about how a seller-funded component of the price is legally structured, whether it creates a competing claim over the business or sits as a plain contractual obligation. I have written about that distinction separately, because getting the wording wrong there can make an otherwise fundable deal unbankable.

What is vendor finance?

Vendor finance is a loan arrangement between the buyer and the seller. The seller agrees to receive part of the purchase price over time rather than in full at settlement, usually with interest, and becomes a creditor of the buyer's business. In taking on the buyer's execution risk in exchange for a higher eventual return, the seller is signalling confidence that the business will perform under new ownership.

That confidence signal matters to a bank, but so does the legal detail underneath it. If the seller registers a security interest over the business assets to protect the ongoing payment, the bank's own security position now competes with the vendor's. That is the mechanic covered in the deferred payment article, worth reading before you get to heads of agreement stage.

What is bank finance?

Bank finance is a lender advancing funds against the strength of the deal, the security on offer (a general security agreement over the business, property, or both) and the buyer's ability to service the debt from the cash flow of the business being acquired. A bank runs its own credit assessment independent of what the vendor is prepared to offer. Its approval turns on the numbers standing up on their own, not on the seller's confidence in the business.

Bank finance is the larger, more standardised piece of most acquisition capital stacks, and the piece with the least room to move. A lender's serviceability test does not flex because the seller believes in the business.

How do the two combine in a real deal?

In a typical structure the buyer brings a cash contribution, generally around 30% of the purchase price where no property is offered as security, though this moves lower when property support is available. The bank funds the largest share against security and serviceability, which you can size early with our business acquisition calculator. Any gap between what the buyer can contribute and what the bank will fund is where a vendor component often gets discussed.

The trap buyers fall into is assuming that gap can be filled with vendor finance and that this improves their equity position, when it does not. Banks treat vendor finance as additional debt sitting behind their own, not as buyer equity, and the ongoing vendor repayments still count against the business's servicing capacity. A gap-filler structured as vendor finance can weaken a deal in front of a credit team rather than strengthen it.

This is why, on nearly every acquisition I work through, the conversation moves toward reshaping the vendor component into something a bank reads more favourably: an earn-out tied to revenue, or a deferred payment with no competing security. Same money and timeline to the seller, but a different characterisation and a different outcome at credit assessment. The mechanics of that reshaping are the subject of the deferred payment article.

"A seller willing to leave money in the business is a real alignment signal, and I will say so when I take a deal to a lender. At the same time, the bank's own general security agreement sits behind a competing creditor if the vendor has registered an interest, and major banks in particular will generally not proceed on that basis."

What does a bank actually think when vendor finance shows up in a deal?

A bank reads vendor finance two ways at once. A seller willing to leave money in the business is a real alignment signal, and I will say so when I take a deal to a lender. At the same time, the bank's own general security agreement sits behind a competing creditor if the vendor has registered an interest, and major banks in particular will generally not proceed on that basis. Challenger lenders show more flexibility case by case, and private credit tolerates more complex seller-funded structures, though usually only above a certain deal size and at a higher cost of capital.

My practical guidance to buyers is to have this conversation with a broker before the heads of agreement is drafted, not after. Restructuring a vendor component once the documentation exists is a legal exercise. Getting the structure right before that point is a conversation.

If you are working through how to fund an acquisition and want to talk through where the vendor component sits in your structure, that is exactly the conversation to have with us before the heads of agreement is drafted. As your broker, we structure the capital stack around the vendor and bank components, then take the bank-funded portion to the lenders across the Big 4, challenger banks and private credit whose appetite fits, so you are represented to several at once rather than approaching one lender cold. See how we approach acquisition finance, or book a call and we will come back to you with next steps.

Frequently asked questions

Vendor finance is money the seller agrees to leave in the deal, repaid by the buyer over time as a creditor arrangement. Bank finance is money a lender advances against security and the business's ability to service the debt. One comes from the person selling the business, the other from an institution assessing the deal on its own terms.

Yes, and most acquisitions combine both alongside the buyer's own cash contribution. The bank funds the largest share against security and serviceability, and a vendor component fills part of the remaining gap, usually reshaped as a deferred payment or earn-out so it does not compete with the bank's security.

It can do either, and the structure decides which. A seller leaving money in the deal is a confidence signal a bank will note. If that arrangement carries a registered security interest for the vendor, it creates a competing claim over the business that most banks, particularly the major banks, will not accept alongside their own.

This article is general information and does not constitute financial or legal advice. Funding structures vary deal to deal, and the right mix of vendor and bank finance depends on your circumstances. Speak to your broker before the heads of agreement is drafted.

Working out your funding mix?

If you are looking at a business and want to understand how much of the purchase a bank will fund versus what needs to come from the seller or your own contribution, tell us about the deal. We will walk through the structure and the lenders most likely to support it.