Last updated: July 2026

What banks look for in business acquisition loans (and why the majors got harder in 2026)

Why are the major banks getting selective on business and commercial lending?

The plain version is that the majors have been managing their capital more tightly since the Basel III output floor came into full force in 2026, and business and commercial lending is where that discipline shows up first. Basel III sets how much capital a bank has to hold against every loan it writes, and how much depends on how the regulator risk-weights that loan. The majors have responded by raising the bar on the loan types that consume more of that capital, and getting more deliberate about where the rest of it goes.

Every loan a bank writes has to be backed by capital, and the amount of capital scales with how risky the regulator judges the loan to be. This is the risk-weighted assets, or RWA, part of the equation, and it is where business and commercial lending is capital-intensive relative to a mortgage. Under the Basel III output floor now in force, a standard mortgage carries only about a 7 percentage point increase in risk weight, while rated corporate lending carries about 37 percentage points. A commercial or acquisition loan therefore consumes far more of a bank's capital than a home loan does, which is why it is the first place a bank raises the bar when it is being selective.

You can already see it in the guidance. NAB told the market it expected second-half business credit growth to slow from 10 per cent a year to about 6 per cent, the first clean "we are dialling back" signal of the reporting season. The pullback is showing up through capital allocation and provisioning posture rather than a headline rule change, which is why a lot of borrowers feel the ground shift without being able to point to what moved.

What do banks look for in a business acquisition loan now?

Demand for credit has not softened, which is worth saying plainly. Business credit was still running at 9.6 per cent a year in April. The appetite to borrow is there, the supply of easy bank approvals is what has tightened. So the bar to clear at a major is higher, and it clears on the fundamentals I have always cared about, applied more strictly.

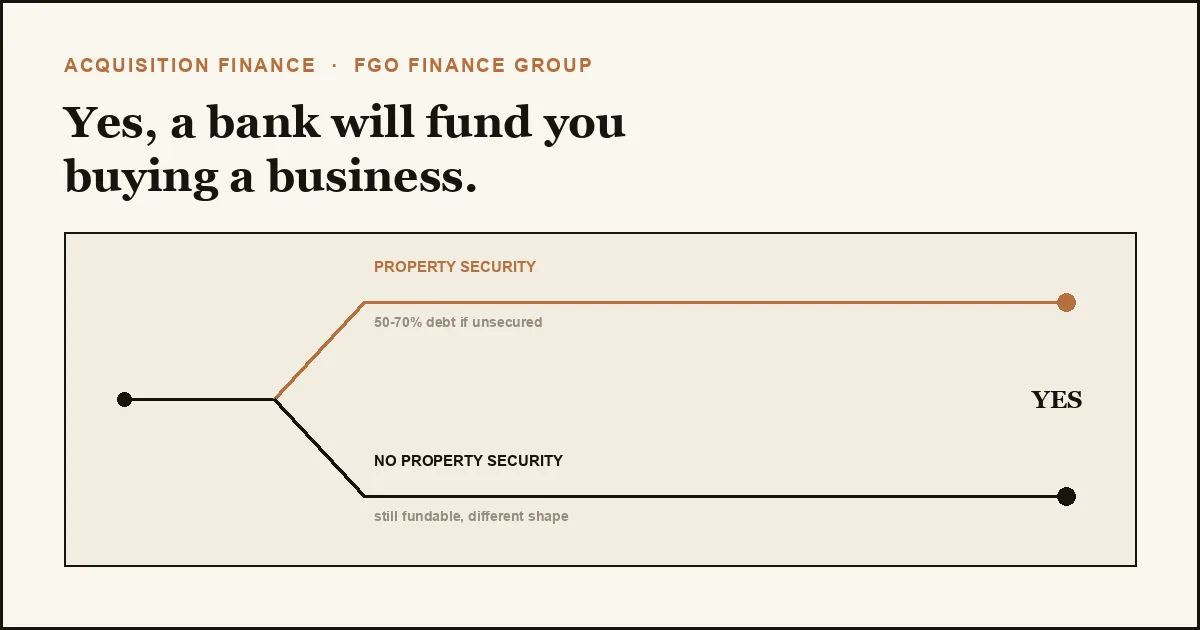

Banks want to see serviceability that holds at today's rates, not a rate you are hoping to refinance into. With the RBA's terminal rate now expected to reach 4.60 per cent around August and sit there into 2027, the "wait for cuts" thesis does not help a credit assessment. They want a clear second way out, meaning security or a repayment path that protects the lender if trading disappoints. For an acquisition, they want to understand the quality and durability of the earnings you are buying, the price you are paying against those earnings, and how much of your own capital sits alongside the loan. They want the goodwill component structured sensibly, because goodwill is the piece a bank is least comfortable lending against. None of this is new. What has changed is that a bank managing its capital more tightly now says no to a deal it might have stretched for a year ago, and it says no more quickly.

The practical read for a buyer is to bring the deal to the table already structured for how credit teams think. Clean financials, a defensible valuation, a genuine equity contribution, and a repayment story that survives a flat trading year. That preparation is where a broker earns their keep, and it is most of what we do before a deal ever reaches a lender.

"A no from one major is a data point, and it does not mean the deal is unfundable. It usually means the deal did not fit that bank's current capital appetite, which is a different thing from the deal being weak."

Where do acquisition and commercial deals get funded when a major says no?

When the majors tighten, the funding moves to where capital constraints bind less. That is the challenger lenders and the private credit market. Challenger banks and non-bank lenders often price higher than a major, and they carry their own capital limits to watch, so this is not an easy route. What they offer is appetite for the exact RWA-heavy business and commercial exposures the majors are stepping back from, and often a faster and more commercial credit decision. For an acquisition that is sound on the fundamentals but does not fit a major's box this year, that flexibility is frequently the difference between settling and stalling.

Knowing which lender is leaning in on which type of exposure this quarter is the whole game in a market like this one, and it changes month to month as each lender's own capital position moves. That is the part of the market FGO watches closely, and it is the guidance we bring to a buyer trying to work out where their deal actually gets funded. As your broker, we take a deal to several lenders across the Big 4, challenger banks and private credit at once, matched to whoever currently has appetite for it, rather than leaving you to test one bank's current risk settings on your own. For the wider picture on funding a deal, see our guide on acquisition finance, or read how we approach commercial finance more broadly.

Frequently asked questions

Yes, and demand is strong, with business credit growing 9.6 per cent a year as of April 2026. The majors have become more selective on capital-heavy business and commercial loans as they manage their capital more tightly under Basel III, so approvals at the big banks are harder to win. The lending is still there, it is more concentrated in well-structured deals and in the challenger and private credit lenders.

A bank must hold capital against every loan, and the amount scales with how risky the regulator judges the loan to be. That measure is the risk-weighted asset. Business and commercial loans carry much higher risk weights than mortgages, roughly a 37 percentage point increase for rated corporate lending versus about 7 for a home loan under the current Basel III floor. When a bank is being more selective with its capital, the high-risk-weight loans are the first it raises the bar on, which is why acquisition and commercial borrowers feel it first.

No. A major declining a deal often reflects that bank's capital appetite this quarter rather than a flaw in the deal. Challenger lenders and private credit sit outside the tightest of those constraints and actively want the business and commercial exposures the majors are stepping away from. The task is matching the deal to the lender who has appetite for it right now.

This article is general information and does not constitute financial or legal advice. Your circumstances and the lending market both change, and the right approach depends on your deal. Speak to a broker before you take a single bank's answer as final.

Financing a business acquisition or commercial property this year?

If you want to understand where your deal actually gets funded in this market, tell us about it. We will walk through the structure and the lenders most likely to have appetite for it right now.